The Rate Cuts Are Coming! The Rate Cuts Are Coming!

The Rate Cuts Are Coming! The Rate Cuts Are Coming!

By: Erik Conrad, CEO of InCommercial

The fog of conflicting economic data reminds me of an observation a colleague once shared with me – there is no difference between being demonstrably wrong and having bad timing.

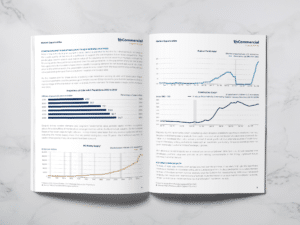

The data released in early June 2024 highlight the seemingly contrasting data from the Bureau of Labor Statistics and the challenges facing the Federal Open Market Committee. This is the U.S. Federal Reserve’s rate-setting committee, or FOMC. The noise, however, does not make the consequences of bad timing any less severe, and the signals are increasingly pointing to the need for a policy shift sooner than later. Much like my colleague’s observation, the FOMC will either ease rates soon or aggressively cut rates rapidly later. So, let’s examine the signals and shine a light on a clearer portrait of the American economy.

If just one basic underpinning of the data is adjusted – total population figures – the incongruent data is corrected. This sounds the alarm for a policy path to ease rates and prevent a severe recession or ensuing deflationary cycle.

- June 7, 2024: BLS reports the household and establishment survey results, which point in opposite directions:

- The establishment survey – a survey of employers – suggests 272,000 jobs were added in May 2024, well above consensus estimates.

- The household survey – a survey of households – reports 408,000 fewer jobs for the month with unemployment rising to 4%.

- Year-over-year job creation in the establishment survey: 2,756,000

- Year-over-year job creation in the household survey: 376,000

- June 12, 8:30 am ET: BLS reports that May’s Consumer Price Index was unchanged for the month, in other words, a 0% increase in the CPI for the month and 3.3% for the year.

- June 12, 2 pm ET: The Federal Reserve holds rates steady for June and revises guidance from two rate cuts to one for the remainder of the year.

- June 13: BLS reports that May’s Producer Price Index was down 0.2% in May and up 2.2% for the year.

Looking back over the past 24 months, headline CPI has decreased from a 9.1% annual rate to 3.3%, as measured year over year. The Federal Reserve’s explicit target is 2% as measured by the Personal Consumption Expenditure, which is structurally 0.5-1% lower than the CPI and currently reading 2.6%. The focus on the PCE, despite frequent media spin, is not because it is lower than the CPI; it’s because it’s a better measure of the impact of higher prices on consumers:

- CPI measures a basket of goods and tracks increases in prices of those goods over time; and

- PCE measures the expenditures of households on goods and, therefore, captures the changes in behavior that come from higher prices.

For example, brand-name eggs cost more so consumers buy a larger share of store-brand eggs as prices rise. Eggs are more expensive, and CPI captures that growth. Consumers choose the cheaper alternative more often, so in the aggregate, the growth in expenditures is lower.

I’ve written, posted, and lamented about much of this before:

- Getting CPI from 9.1% to 3.3% doesn’t require the same policy as 3.3% to 2% regardless of how you interpret the leading indicators. The decision not to ease into the correct rates with gradual adjustments will no doubt require more aggressive action in the future. The economy is often referred to as a cruise ship; I’ve never captained a cruise ship, but I know that you don’t wait till you hit the pier before easing off the throttle.

- The largest contributor of inflation continues to be shelter, in fact, the PCE excluding shelter has been below target on a year-over-year basis (even lower using shorter-term measures and projecting forward) for over nine months! Estimates of shelter costs are intrinsically flawed, delayed, and tend to bias upward during periods of higher rates because housing is so intrinsically tied to mortgage costs.

- There is no recorded period when the labor market softened by the Federal Reserve’s target of 0.5% without continuing to degrade by at least 2%. In other words, we doubt the forecast, because it has never been achieved (prior performance not being indicative of future results of course). The American job market has actually achieved that 0.5% increase in unemployment having moved from 3.5% to 4% and history suggests we are therefore on the precipice of a broader decline and recession.

These are not the only reasons why I’m convinced that rate cuts are coming and concerned about how far behind the curve the FOMC finds itself once again. The strength in the job market and the gross domestic product figures are illusory, masking a building underlying issue that is apparent in other data.

Consumers and businesses alike feel negatively toward the economy in spite of strong jobs and GDP numbers. In response, there seems to be a steady feed of articles inventing explanations for why people feel poorly about the economy despite clear and convincing evidence that they are wrong. Maybe people know how they’re doing and feeling, and maybe, just maybe, they’re right and the data isn’t telling us an accurate story.

The only relevance to the number of jobs created each month is how it impacts households. The survey results stated above clearly indicate that the labor market, as it impacts households, is fairly negative. Approximately 100,000-200,000 jobs need to be created every month to keep up with the growth of the working-age population. Therefore, job creation above those numbers is worrisome when unemployment is already low.

The relationship of the job creation figures to the neutral rate is its only significance – if the neutral rate were 500,000, a number below that figure would be deflationary as more workers competed for fewer jobs and it would take a number over 500,000 to be inflationary. The monthly job creation figures are completely irrelevant without understanding what number is neutral.

What happens if we experience a period of extraordinary immigration, like say, right now? Currently, the Census Bureau (used in BLS calculations) immigration estimates stand at 1.1 million annually but the Congressional Budget Office (not used in BLS calculations), based on data collected at the border by the U.S. Department of Homeland Security, suggests the number is actually 3.3 million annually. Would some percentage of those extra 2.2 million people need to work and therefore the neutral rate of necessary job creation indeed be closer to 350,000 or 400,000 people rather than 150,000 people? Could those numbers easily explain a significant piece of the discrepancy between household and establishment surveys?

- Establishment survey: Survey a representative sample of employers and then benchmark to the number of employers (i.e., survey 1% and then multiply by 100 to get the raw numbers).

- Household survey: Survey a representative sample of households and then benchmark to the total households in the population (i.e., survey 1% of households and then multiply by 100 to get the raw numbers).

The two surveys are different, and on a month-to-month basis they don’t need to match but historically converge because they are trying to measure the same thing: employment. The surveys have been diverging for over two years (roughly the period of hyper-immigration that we have been experiencing post-COVID).

Employers register with the IRS, so those numbers are presumably known. The Census Bureau numbers appear demonstrably wrong for several years. The unemployment rate is likely correct (because it is a ratio that should be the same in the subset as the total), but the number of total jobs is structurally wrong if the population estimate is wrong.

The household survey is incorrect because it should be benchmarked to a larger population. There are more jobs than indicated but at the same time, it is accurate that people are feeling stressed and there aren’t enough jobs for people who want them. The unemployment rate is increasing, and workers are feeling the pressure.

It is troubling how easily the “strength” data points can be explained by this larger population, compared to what the BLS acknowledges. Even if recent data suggests a weakening consumer and slowing GDP, this should be viewed in the context of data that, before now, has been seen as surprisingly strong and resilient. But again, this data is being expressed in raw size – i.e., the size of GDP is growing in nominal terms, and the consumer is buying more than last year in nominal terms. The issue here is that every single person is incrementally accretive to these figures so a larger population on the scale of several million people each year easily tips the balance.

More people means a larger economy by default and more consumption by default, but growth in GDP below population growth is a signal of declining quality of life and deflationary. So, when that same data is being portrayed as its opposite, I get very concerned about the resultant policy response. Depressions were a relatively common occurrence before the modern-day Federal Reserve, and they have been largely attributed to the wrong policy response: bad medicine. I am explicitly not making a value judgment on policy or any people; this is only about the data giving us the wrong signal.

As the data converges, it points to a softening of inflation, demand, and the labor market. When the leading indicators point to further softening, if not outright decline, rate cuts should follow. If the FOMC continues to hold rates past the election or into next year, I fear it will be too late. The Federal Reserve’s dual mandate is full employment and price stability and while some signals for both price growth and labor market show limited strength, the direction for both is abundantly clear. The FOMC doesn’t need to change its measurements or data, but it can take in the signals, understand them, and react accordingly.

Both price stability and full employment are at risk in the current environment as deflationary forces have an opportunity to set in amidst a labor market that is rapidly softening. The economy operates best in a relatively small window. Inflation builds on itself and can spike (as we’ve all experienced) if it moves beyond a typical range. The labor market similarly degrades rapidly when the economy is pushed into a recession. Layoffs decrease demand rapidly, which in turn leads to more layoffs. Inflation may be bad, but deflation is worse. Everyone would like lower prices, but lower prices (deflation) are a doom loop for the economy as they further suppress consumer demand (waiting for even lower prices).

Declining prices pose significant problems for businesses that typically cannot cut wages and therefore lay off employees, creating a vicious cycle. Further, the FOMC policy prescription for inflation is relatively simple as there is no upper bound to the interest rate that can be set. However, the same cannot be said for a deflationary spiral, as rates cannot be set materially below the zero lower bound.

With an inflation target as low as 2% and the economy well on its way to that target (if not past it), the risk of tipping the economy into a deflationary spiral is becoming increasingly real.

I’ve always thought two hands and one lantern were sufficient to find the right policy, but we now have ample hands, and multiple lanterns, and still can’t find the correct path. The rate cuts are coming, it’s just a question of whether it will be enough by the time they arrive.

Erik Conrad is the founder and chief executive officer of InCommercial Property Group – a full-service, end-to-end investment real estate portfolio manager. He has led real estate companies for over 20 years and has 22 years of licensed real estate brokerage experience, as well as involvement in over 2,000 net-leased real estate transactions.

InCommercial is a full-service, end-to-end investment real estate portfolio manager with deep subject matter expertise. Through a 20-year history, its experienced team is dedicated to creating demonstrable value by leveraging their long-standing industry relationships to attempt to create value at each step of the investment cycle starting at acquisition and continuing through streamlined operations, accretive financing, and efficient exits.

Read the full article on DI Wire here:

https://thediwire.com/the-rate-cuts-are-coming-the-rate-cuts-are-coming/

Texas Property Acquired for Motor Fuel Fund III Offering

InCommercial Acquires Texas Property for Motor Fuel Fund III Offering

InCommercial Capital Corporation announced the acquisition of a retail motor fuel outlet, a Chevron service station with a Quick Stop convenience store.

InCommercial facilitated the acquisition of the property on behalf of InCommercial Motor Fuel Fund III, LP. The fund launched a 506(c) private placement offering last month, seeking to raise $50 million from accredited investors interested in the potential for tax advantages through the use of leveraged bonus depreciation.

The Chevron service station and Quick Stop convenience store are located in Houston, Texas, at Mohawk Street and Homestead Road intersection. The acquired property was built in 2019 and includes a 9,820-square-foot building on 1.47 acres. The new lease is a 20-year absolute triple net lease agreement with Panthers Petroleum, the tenant and corporate guarantor. The Texas-focused company has over a 25-year history in the gas station, retail, and wholesale service industry.

“We’re particularly excited about acquiring this recently developed build-to-suit property with a long-term lease commitment. Acquiring an asset that is a few years old versus several decades old makes a big difference in terms of future maintenance and repair costs,” said Andrew Haleen, acquisitions director for InCommercial.

“The facility’s fuel infrastructure and fresh design are inviting and provide an elevated feel for its customer base. The site is a prime example of our commitment to our investors and the fueling experience,” added Haleen.

InCommercial is a full-service, end-to-end investment real estate portfolio manager with deep subject matter expertise. Through a 20-year history, its experienced team is dedicated to creating demonstrable value by leveraging their long-standing industry relationships to attempt to create value at each step of the investment cycle starting at acquisition and continuing through streamlined operations, accretive financing, and efficient exits.

Read the full article on DI Wire here:

https://thediwire.com/incommercial-acquires-texas-property-for-motor-fuel-fund-iii-offering/

The Golden Age of Net Lease?

The Golden Age of Net Lease?

By: Erik Conrad, CEO of InCommercial

By now, it’s old news that interest rates have increased dramatically. The Federal Reserve in the recent tightening cycle hiked rates faster and farther than any period in the past four decades. But that wasn’t even the only bank-related pressure on commercial real estate as the Federal Reserve also reduced the money supply more quickly than in the last six decades and proposed significant capital requirements for banks known as Basel III Endgame.

The last few years have been a hard time to be in commercial real estate, but it’s been even harder to be a lender in the space – lenders, who rely on loan payoffs to recycle the capital into new loans don’t get many payoff requests when they have loans on the books at 3% to 4% and savings accounts are paying 5% or more!

Another major source of debt capital for commercial real estate is commercial mortgage-backed securities and other asset-backed securitized loans. For those unfamiliar, these are loans that are packaged together and sold off as bonds by the banks for fixed durations. At its core, a lender makes a loan and then slices it up and sells the loan for a small markup in the form of bonds to bond buyers. It works great for the banks when interest rates are stable and breaks when interest rates move quickly because the value of the bonds aren’t stable enough to have certainty around profit margins. In theory, banks aren’t supposed to take that kind of risk, and interest rates have been anything but predictable over the past two years.

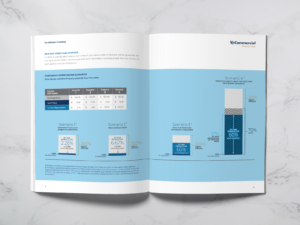

So here we are, debt issuance for commercial property acquisitions in 2023 was roughly at 2011 levels without adjusting for inflation, and yet most commercial real estate with the notable exception of multifamily, is at or very near its peak value (to say nothing of the stock market which is at or near all-time highs as well).

How can it be that with all the fundamental demand for housing, multifamily is the asset class most impacted by interest rates? Isn’t multifamily supposed to be able to absorb the market adjustments and increase rents to deliver investor returns in any market? That’s what I’ve always been told (though unfortunately never experienced).

What can explain these divergent experiences with retail properties and net leased properties? How can net lease experience stable values in the face of high interest rates and constrained capital while multifamily experiences a massive adjustment in values under the same conditions? It’s even more confounding when one considers the quasi-government agency liquidity and sub-market debt pricing bestowed upon multifamily as an essential asset and a societal good.

THEORY 1: Price Adjustments Are Still to Come

It’s possible that thanks to the government-subsidized liquidity in the multifamily market there has been more “price-discovery” so we’re seeing the impacts of higher rates translate to values in that asset class before other asset classes for which very little capital is available. In fact, office property values show far more stability than one might expect given the poor utilization, lack of liquidity, and heavy cost of operations in that asset class. If we can’t predict when office demand will stabilize by employers and users, it’s hard for price discovery to occur.

The data, across asset classes, show transaction volumes consistently impacted over the past several years, with office being notable in its lack of transactions since the start of the pandemic rather than associated with the tightening cycle. The argument that there is more price discovery can’t explain what we’re experiencing, and the answer must lie a little deeper – more fundamental.

THEORY 2: Current Rates Are Temporary, Projected Income Is Driving Values

Commercial real estate is a long-term investment and regardless of a particular investor’s investment horizon, a serious investor will be evaluating the investment on a 20-year or longer investment horizon. After all, even if you have a five-year horizon, your buyer will be looking into the future. Real estate isn’t consumer electronics, we build permanent structures intended to be used for decades and so that must be our evaluation period.

Most people think of interest rates in terms of their home and a 30-year mortgage. That experience, unfortunately, is not very helpful when assessing commercial real estate which is often financed with five- or 10-year loans. So, the logical conclusion on a 20-year investment and a five-year loan means the investor is really looking at long-term rate expectations and not as focused on the rate quoted today. Today’s rate and availability are important, but is it 10%, 20%, or maybe 30% important? It certainly isn’t higher than that for any rational investor or you’re risking getting well over your proverbial skis.

Multifamily, through various government agency-sponsored debt providers, has experienced less debt and liquidity disruption than net lease, so why then is the valuation change so much more dramatic? What’s the other variable in the value equation that might explain the difference?

The remaining variable is the projected income and that is where net leased properties can impress or bore you depending on your perspective. In 2020 and 2021, rents in multifamily were driven by easy money, stimulus, and work-from-anywhere policies, which also drove inflation to rates unseen in decades. In 2022 and 2023, those drivers have reversed, and the ensuing inflation is hitting the insurance, property taxes, and maintenance expenses that multifamily operators now need to absorb while rent growth stagnates and retreats. The projected income has declined dramatically and that explains the retreat of values in multifamily in most cases.

What happened over that same period in net lease? Nothing to speak of. Some markets have fallen out of favor; urban store closures are inevitable when political winds create bad retail environments. Retailers don’t want to operate in locations where their customers and employees don’t feel safe but high-profile store closures obscure the underlying trend of increased store openings and renewed retailer reliance on brick-and-mortar locations. Outside of retailing 101, construction costs are way up, and inflation has created a dynamic where tenants with long-term leases have so much value in their existing leases, a lower cost structure, lower taxes, and lower insurance such that relocating to the next shiny development rarely makes sense. Meanwhile, as an investor in net lease, the renewal rates have all increased, the income is unchanged (whatever the lease always had), the expenses are the tenant’s issue, and even those are being paid via inflation-diluted dollars.

Renewal rates have gone up (primary risk driver down), the income is stable and the long-term outlook for interest rates (Federal Reserve Target) is essentially unchanged. This leads to the conclusion that the intrinsic value of net leased properties has increased – same income, lower risk – over the past two years.

THEORY 3: Interest Rates Are Masking a Huge Demand Shift to Net Lease

The premise here is that interest rates, liquidity, and all the aforementioned factors are impacting values equally across asset classes. In a supply and demand model of the investor economy, the difference in valuations must be that more investors are choosing to invest in or hold onto their net lease properties and are more interested in selling off or steering clear of multifamily. The reason could be many of the same drivers already discussed, along with the massive retirement and wealth transfer occurring as boomers retire and wealth concentrates leading more and more investors to stable bond-like returns. Those bond-like returns can be found in net lease of course, but they are also found in … bonds, which further lowers borrowing costs and ultimately supports net leased properties either way.

This theory implies that as interest rates start to fall and multifamily prices stabilize, net lease values soar to new heights as investor demand is unleashed by lower rates against a limited supply of suitable investments.

CONCLUSION: Where Do We Go From Here?

We buy into the second theory that interest rates are only modestly determinative of values and today presents a significant buying opportunity. We’ll be pleasantly surprised if the third theory is correct, and demand is overwhelming in the years to come. Lastly, we stay focused on building robust income streams with manageable debt levels.

Sellers in today’s market are selling due to external and, dare we say, transitory factors. Valuations have held so strongly because the projected income variable has increased with the higher likelihood of renewals and rent bumps while the long-term interest rate projections are unchanged. If anything, the current interest rate environment and lack of debt capital have masked what is otherwise a bull run in values for this asset class.

When an investor wants to feel the market and take the ups and downs, multifamily makes a lot of sense, but a larger and larger percentage of today’s and tomorrow’s investors are going to want to mute that volatility in favor of stable and predictable income streams. A growing share of American investors are going to purchase bonds, driving down borrowing costs, and net leased properties in pursuit of some extra returns with stability. These bond-like assets are likely to deliver outsized returns for several years to come as we enjoy both current income and asset appreciation from long-term trends being unleashed as the Federal Reserve eases off its restrictive policies.

InCommercial is a full-service, end-to-end investment real estate portfolio manager with deep subject matter expertise. Through a 20-year history, its experienced team is dedicated to creating demonstrable value by leveraging their long-standing industry relationships to attempt to create value at each step of the investment cycle starting at acquisition and continuing through streamlined operations, accretive financing, and efficient exits.

Read the full article on DI Wire here:

https://thediwire.com/guest-contributor-the-golden-age-of-net-lease/

InCommercial Launches Motor Fuel Fund III Offering

InCommercial Launches Motor Fuel Fund III Offering

InCommercial Capital Corporation announced its newest limited partnership offering: InCommercial Motor Fuel Fund III, LP. The fund is seeking to raise $50 million from investors who are interested in the potential for tax advantages through the effective use of leveraged bonus depreciation.

The fund will invest primarily in gas stations and convenience stores that qualify as Retail Motor Fuel Outlets under the U.S. tax code. By qualifying as Motor Fuel Outlets, the fund is eligible to utilize bonus depreciation to create passive losses. This allows investors in the fund to potentially offset taxes on passive gains. This tax strategy – according to InCommercial – would be an ideal solution for cash flow from a portfolio of real estate holdings, the sale of a business, or resolving a stalled 1031 exchange.

The fund will be offered to accredited investors pursuant to Regulation D, Rule 506(c) under the Securities Act of 1933.

“With all the changes in the retail sector, the opportunities for investment in the convenience and gas sector has never been greater and we’re very excited to combine these strong fundamentals with very compelling tax advantages for qualified investors,” said Erik Conrad, chief executive officer for InCommercial.

Since the launch date of the fund, InCommercial has reported that it is proceeding with its first acquisition – a Chevron in Houston, to be operated by one of InCommercial’s existing operators. Consistent with its investment strategy, the fund will utilize a sale/leaseback transaction to acquire the property and simultaneously lease it under a 20-year, triple net lease to an established operator.

“We are thrilled to be able to continue to support our tenant’s growth in the very competitive Houston market, as well as the potential benefits to all of our investors for this well-positioned property,” said Andrew Haleen, acquisitions director for InCommercial.

The fund has entered into a managing broker-dealer agreement with JCC Capital Markets LLC. The fund will seek to offer shares through both the independent broker-dealer and registered independent adviser channels.

“On the heels of a successful capital raise and execution of acquisition for the InCommercial Motor Fuel Fund II, LP, we look forward to working with our incredible group of [investment banking division] and RIA partners for Motor Fuel Fund III, LP,” said Dan Mercer, Jr., senior vice president of capital markets for InCommercial.

InCommercial is a full-service, end-to-end investment real estate portfolio manager with deep subject matter expertise. Through a 20-year history, its experienced team is dedicated to creating demonstrable value by leveraging their long-standing industry relationships to attempt to create value at each step of the investment cycle starting at acquisition and continuing through streamlined operations, accretive financing, and efficient exits.

Read the full article on DI Wire here:

https://thediwire.com/incommercial-launches-motor-fuel-fund-iii-offering/

Whitepaper: Tax Efficient Investing [Updated Jan. 2024]

InCommercial announces the released update of its whitepaper titled: Tax Efficient Investing – Maximizing the Efficiency of Depreciation.

The whitepaper discusses tax-efficient investing using bonus depreciation, applicability, and usage in today’s market.

Written by Erik Conrad, CEO of InCommercial Property Group.

Download Whitepaper: Tax Efficient Investing [Updated Jan. 2024]

Introduction:

Continuing in the path of 2022 and 2023, 2024 is anticipated to be a difficult time to be an investor in any asset class. Inflation, the great destroyer of wealth, is receding with prices still high along with uncertain economic conditions. Taxes, always a concern for the sophisticated investor, seem only set to rise. That challenging backdrop is met with potentially falling corporate profits, stock market volatility, and declining rental rates in many markets.

To excel in 2024, an investor will have to make smart choices to invest in assets that produce durable income, backed by strong companies in resilient industries while being mindful of how to protect those gains from today’s challenges – including dilution from rising taxes.

Read the full whitepaper HERE: Tax Efficient Investing [Updated Jan. 2024]

Disclaimer:

InCommercial Property Group and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. As mentioned throughout this presentation you should consult with competent, independent, tax representation before engaging in any transaction.

Whitepaper: Market Opportunities

InCommercial announces the release of its latest whitepaper titled: Market Opportunities – Capitalizing on Current Conditions while Hedging Risks.

The whitepaper discusses build-to-suit development strategy, key risks, opportunities, and underwriting in today’s market conditions.

Written by Erik Conrad, CEO of InCommercial Property Group.

Download Whitepaper: Market Opportunities

Introduction:

A “Build to Suit” or “BTS” development is one wherein a commercial property tenant enters into an agreement with a developer or landowner to construct a new, purpose-built facility for the tenant tied to a long-term lease commitment from the tenant once completed. Build to Suit development opportunities are historically amongst the market’s most popular as well as the most limited investment opportunities. Once an investor understands and appreciates the nature of a build to suit development cycle it becomes apparent why, particularly in bull markets, the opportunity to invest in the build to suit space is limited to long-term market insiders.

Build to Suit developments seek to eliminate the speculative variables that accompany most development projects with the largest and most obvious being entitlements and lease-up. The additional certainty from eliminating these substantial risks compresses the development timeframe and drives attractive annualized returns comparable (on an IRR basis) to more speculative investments.

Sophisticated institutional investors and lenders have traditionally crowded out individual investors in this sector because of the high relative risk-adjusted returns and predictable, repeatable business opportunities afforded. The recent monetary tightening, combined with the persistently slower velocity of capital within the commercial real estate market (a result of the Federal Reserve’s efforts to reduce inflation), has resulted in opportunities for investors to capture a share of this attractive development sector and secure long-term gains that are not generally otherwise available.

Read the full whitepaper HERE: Market Opportunities